IFRS S2 | Climate-related disclosures

IFRS S2 shall be applied for annual reporting periods beginning on or after 1 January 2024 (earlier application is permitted, only if IFRS S1 is simultaneously implemented). Disclosures are not required before the date of initial application (the start of the first reporting period), so disclosure of comparative info is not required in the first annual reporting period.

Objective & Scope of IFRS S2

The objective of IFRS S2 is disclose both climate-related risks as well as opportunities, to which an entity is exposed; which are useful to the primary users of financial reports in making decisions related to providing resources to the entity (IFRSS2.1)

(IFRSS2.2) "Climate-related risks and opportunities that could reasonably be expected to affect the entity's prospects" are those which could responably be expected to affect the entity's:

- cash flows;

- access to finance; or

- cost of capital over the short, medium or long term

Climate-related risks & opportunities that could not reasonably be expected to affect an entity's prospects are outside the scope of IFRS S2.

Climate-related risks include both:

Governance disclosures | IFRSS2.5 to 7

An entity's climate-related governance is driven by a governance body, with management have responsibilities delegated to it.

For the governance body the following should be disclosed with respect to how it oversees the entity's climate-related risks & opportunities:

- How it’s reflected in the terms of reference of the body, its mandates, and role descriptions.

- Does the governance body have the necessary skills to respond to risks/opportunities?

- How often is it informed?

- How are risks/opportunities factored into strategy, major transactions and risk management processes? Have trade-offs between risks/opportunities been considered?

- How climate-related targets are set & progress monitored; includin how performance metrics are included in remuneration policies.

With respect to management's role:

- Is it delegated to a specific position or management committee? How is oversight exercised over it?

- Are controls & procedures used to oversee climate-related risks/opportunities? How are these controls & procedures integrated with other internal functions?

An entity should avoid duplication; ie have one single integrated set of governance disclosures; not separate disclosures for each sustainability-related risk and opportunity

Strategy disclosures | IFRSS2.8 to 23

Disclosures regarding strategy are to help users of financial statements to understand the strategy for dealing with climate-related risks & opportunities:

- What risks/opportunities could affect the entity’s prospects? (IFRSS2.10 to 12)

- Current & anticipated impact on entity’s business model & value chain. (IFRSS2.13)

- Effect on strategy & decision-making, including info on climate-related transition plan (IFRSS2.14).

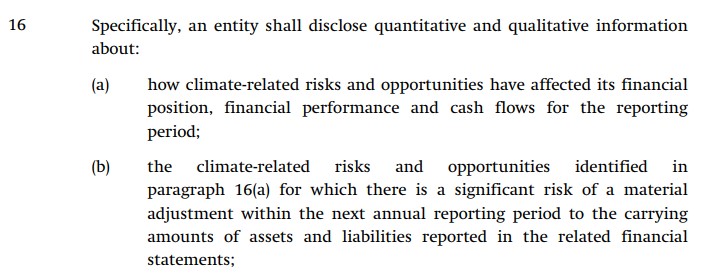

- Effect and anticipated effect on financial position, financial performance & cash flows for the reporting period, over the short, medium & long-term (IFRSS2.15 to 21).

- Resilience of strategy & business model to uncertainties in climate-related changes (IFRSS2.22).

Risks/opportunities affecting prospects | IFRSS2.10 to 12

The first step in the strategy is to identify and describe what climate-related risks and opportunities could affect the business's prospects, whether they are physical or transition risks, and what the time horizon over which the risk/opportunity could realise. This will involve using "all reasonable and supportable information that is available to the entity at the reporting date without undue cost or effort”, and referring to and considering "the applicability of the industry-based disclosure topics defined in the Industry-based Guidance on Implementing IFRS S2”.

Click here to learn more about satisfying the requirements of paragraph 10, 11 and 12 of IFRS S2.

Anticipated impact on business model | IFRSS2.13

Effect on strategy | IFRSS2.14

Effect & anticipated effect on financials | IFRSS2.15 to 21

Resilience to scenarios of climate-related changes | IFRSS2.22

Metrics & targets | IFRSS2.27 - 37

Disclosures help understand an entity's climate-related performance & progression towards internally set or regulated targets. They require:

- info on cross-industry metrics (IFRSS2.29–31);

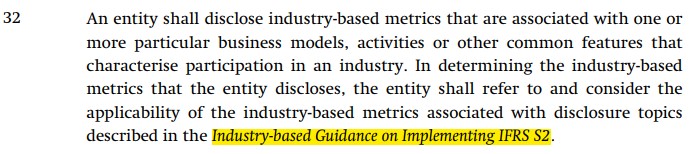

- metrics specific to the entity's industry & activities (IFRSS2.32); and

- targets set by the entity or regulators (IFRSS2.33–37).

Cross-industry Metrics | Paragraph 29(a)

The entity must disclose:

- Greenhouse gas emissions

- Total gross GhG emissions for the period, in metric tonnes of CO2 equivalent (IFRSS2.B19-B22), broken down into

- Scope 1,

- Scope 2

- Scope 3

- Follow the "Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard (2004)" for emission measurement, unless a jurisdictional authority or listed exchange dictates otherwise. (IFRSS2.B23-B25)

- Disclose the approach used to measure GhG emissions (IFRSS2.B26-B29):

- the measurement approach, inputs, and assumptions used,

- the reasons for the selections in (1),

- any changes made during the reporting period.

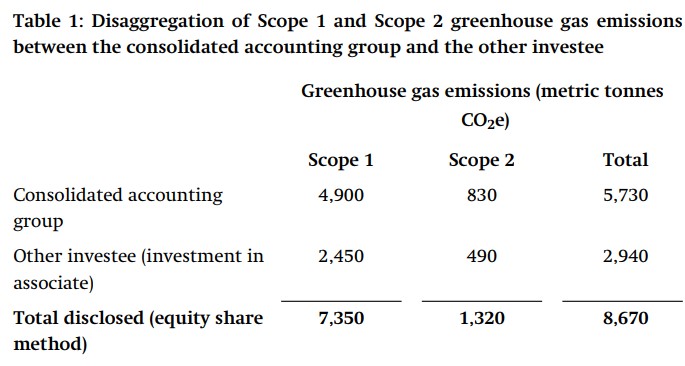

Disaggregate Scope 1 and 2 emissions between the:

Disaggregate Scope 1 and 2 emissions between the:

- consolidated accounting group and

- other excluded investees (e.g. joint ventures, associates & unconsolidated subsidiaries).

- For Scope 2 emissions, disclose location-based emissions and provide necessary contract information to aid understanding.

- For Scope 3 emissions, disclose

- the included categories in line with the "Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (2011)", and

- additional info about Category 15 investment-related emissions ("financed emissions") if the entity’s activities include asset management, commercial banking or insurance (see IFRSS2.B58–B63);

Cross-industry Metrics : Paragraph 29(b)-(g) :

- Disclose the proportion of assets or activities vulnerable to climate-related transition risks.

- Disclose the proportion of assets or activities vulnerable to climate-related physical risks.

- Disclose the proportion of assets or activities aligned with climate-related opportunities.

- Disclose the capital expenditure, financing, or investment deployed towards climate-related risks and opportunities.

- Disclose the entity's internal carbon prices:

- explain whether & how a carbon price is being applied in decision-making (e.g. investment decisions, transfer pricing and scenario analysis); and

- the price for each metric tonne of C02e GhG emissions the entity uses to assess the costs of its GhG emissions;

- remuneration - disclose:

- a description of whether and how climate-related considerations are factored into executive remuneration (see IFRSS2.6(a)(v))); and

- the % of executive management remuneration recognised in the current reporting period that is linked to climate-related considerations.

In prepping 29(b)-(g) disclosures:

In prepping 29(b)-(g) disclosures:

- consider the time horizons over which the effects of climate-related

risks and opportunities could occur (IFRSS2.10)

- consider where in the business model and value chain risks and opportunities are concentrated; e.g.

in geographical areas, facilities or types of assets (IFRSS2.13).

- consider the info disclosed in accordance with

paragraph 16(a)-(b) in relation to the impact of climate-related risks

and opportunities on the entity's financial position, financial

performance and cash flows for the reporting period.

determine whether industry-based metrics, as described in paragraph 32

- including those defined in an applicable IFRS Sustainability

Disclosure Standard or those that otherwise satisfy the requirements

in IFRS S1 - could be used to satisfy the requirements in whole or partially

determine whether industry-based metrics, as described in paragraph 32

- including those defined in an applicable IFRS Sustainability

Disclosure Standard or those that otherwise satisfy the requirements

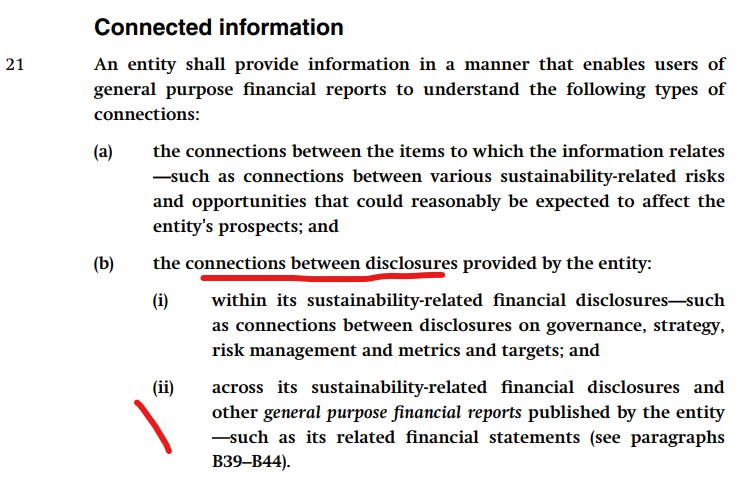

in IFRS S1 - could be used to satisfy the requirements in whole or partially - consider the connections between the info disclosed per:

- paragraph 29(b)-(g) of IFRS S2

- paragraph 21(b)(ii) of IFRS S1

These connections include consistency in

the data and assumptions used and linkages

between the amounts disclosed in accordance with paragraph 29(b)-(g)

and the amounts recognised and disclosed in the financial statements.

For example, is the carrying amount of

assets consistent with amounts included in the financial

statements and what are the connections between info in

these disclosures and amounts in the financial statements.

These connections include consistency in

the data and assumptions used and linkages

between the amounts disclosed in accordance with paragraph 29(b)-(g)

and the amounts recognised and disclosed in the financial statements.

For example, is the carrying amount of

assets consistent with amounts included in the financial

statements and what are the connections between info in

these disclosures and amounts in the financial statements.

Examples of metrics

These examples of metrics paragraphs 29(b)-(e) disclosures are from chapter C of the Task Force on Climate-Related Financial Disclosures, and were copied from there into IFRS S2's accompanying guidance.

| Metric category |

Example unit of measurement |

Example metrics |

Transition Risks: Amount and extent of assets or business activities vulnerable to transition risks

|

Amount and percentage

|

• Volume of real estate collaterals highly exposed to transition risk

• Concentration of credit exposure to carbon-related assets

• Percent of revenue from coal mining

• Percent of revenue passenger kilometers not covered by Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA)

|

Physical Risks: Amount and extent of assets or business activities vulnerable to physical risks

|

Amount and percentage |

• Number and value of mortgage loans in 100-year flood zones

• Wastewater treatment capacity located in 100-year flood zones

• Revenue associated with water withdrawn and consumed in regions of high or extremely high baseline water stress

• Proportion of property, infrastructure, or other alternative asset portfolios in an area subject to flooding, heat stress, or water stress

• Proportion of real assets exposed to 1:100 or 1:200 climate-related hazards

|

Opportunities : Proportion of revenue, assets, or other business activities aligned with climate-related opportunities

|

Amount and percentage |

• revenues from products or services that support the transition to a lower-carbon economy

• net premiums written related to energy efficiency and lower-carbon technology

• number of (1) zero-emissions vehicles, (2) hybrid vehicles and (3) plug-in hybrid vehicles sold

• proportion of homes delivered certified to a third-party, multi-attribute, green-building standard |

|

Capital Deployment : Amount of capital expenditure, financing, or investment deployed toward climate-related risks and opportunities

|

Reporting currency |

• Percentage of annual revenue invested in R&Dof low-carbon products/services

• Investment in climate adaptation measures (e.g., soil health, irrigation, technology) |

Industry-specific & activity-specific metrics | IFRSS2.32

Businesses should share industry-specific measures related to their activities or unique features. When deciding which measures to share, they should use the guidance provided in the 'Industry-based Guidance on Implementing IFRS S2' document as a reference.

Targets set by the entity or regulators | IFRSS2.33–37

Impracticability | IFRSS2.B57

The term "impracticability" frequently surfaced in discussions surrounding IFRS17, particularly in relation to the execution of a fully retrospective approach (FRA). Auditors, understandably, were keen to ensure this wasn't use as a "cop-out". Similar dynamics may emerge under IFRSS2 as it has its own "impracticability" test, specifically targeting the measurement of scope 3 emissions (B57):

"This Standard includes the presumption that Scope 3 greenhouse gas emissions can be estimated reliably using secondary data and industry averages. In those rare cases when an entity determines it is impracticable to estimate its Scope 3 greenhouse gas emissions, the entity shall disclose how it is managing its Scope 3 greenhouse gas emissions. Applying a requirement is impracticable when the entity cannot apply it after making every reasonable effort to do so."

IFRS S2 standard and other reference documents

Click here.