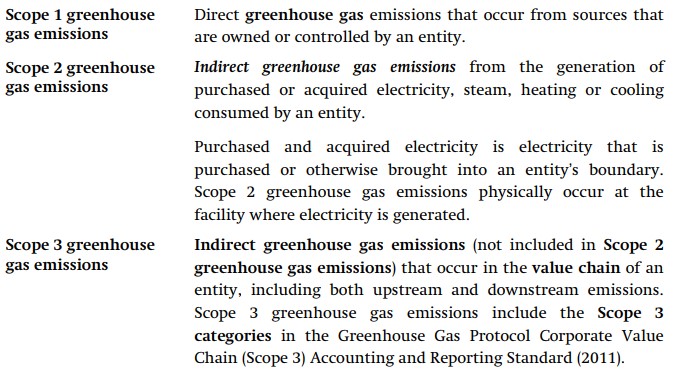

Scope 1 greenhouse gas emissions are defined in the IFRS S2 standard as being "Direct greenhouse gas emissions that occur from sources that are owned or controlled by an entity."

Scope 1 greenhouse gas emissions are defined in the IFRS S2 standard as being "Direct greenhouse gas emissions that occur from sources that are owned or controlled by an entity."See IFRSS2.29 and definitions

Scope 1 greenhouse gas emissions are defined in the IFRS S2 standard as being "Direct greenhouse gas emissions that occur from sources that are owned or controlled by an entity."

Paragraph 29(a)(i)(1) requires the disclosure of Scope 1 greenhouse gas emissions during the reporting period, expressed as metric tonnes of CO2 equivalent; where the emissions of greenhouse gases other than CO2 are translated into tonnes of CO2 which would have the equivalent global warming potential. The 7 constituent greenhouse gases which are aggregated in this manner are listed in the Kyoto Protocol:

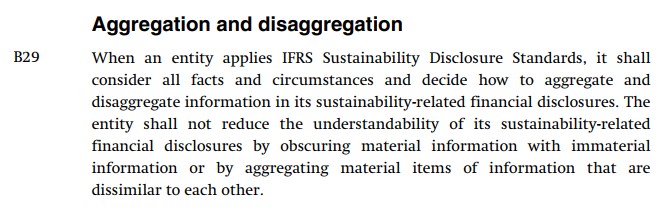

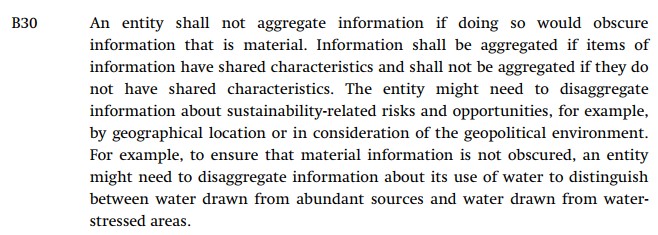

IFRS S2 does not require the disaggregation of the constituent greenhouse gases, but an entity is required to apply the principles of disaggregation and aggregation as set out in IFRSS1.B29 and IFRSS1.B30; with it being key not to reduce the understandability of disclosures by aggregating material items that are dissimilar to each other.

Let's consider an entity in the automotive industry which emits nitrous oxide (N20, an odourless, coloiurless, non-flammable gas; sometimes known as "laughing gas"):

Although IFRS S2 does not explicitly demand an individual breakdown of greenhouse gases, the entity, in keeping with the provisions of IFRS S1, avoids grouping vital data in a way that would conceal critical information. As a result, they elect to offer a detailed account of their primary nitrous oxide emission.

In line with the rules set out in paragraph 29(a) of IFRS S2, the enterprise presents a comprehensive account of its greenhouse gas emissions. To add to the transparency of this disclosure, a supplementary table outlining its primary greenhouse gas emissions is provided. This action attests to the enterprise's pledge to transparency and sustainable environmental practices.