Financed emissions | IFRS S2

See IFRSS2.29, definitions, B58 to B63

An entity lending or investing money, attributes a portion of an investee's or counterparty's gross greenhouse gas emissions to its loans and investments: "financed emissions" are part of Scope 3 Category 15 (investments) as defined in the "Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (2011)".

An entity lending or investing money, attributes a portion of an investee's or counterparty's gross greenhouse gas emissions to its loans and investments: "financed emissions" are part of Scope 3 Category 15 (investments) as defined in the "Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (2011)".

Entities involved in financial activities face risks and opportunities linked to the greenhouse gas emissions of their activities. Counterparties, borrowers or investees with high emissions may pose risks due to technology changes, supply-demand shifts, and policy changes; which in turn may impact the entity's credit, market, reputational or operational risks.

For instance, credit risk may stem from stringent carbon taxes or technology shifts, while reputational risk can result from financing fossil-fuel projects. Therefore, financial entities manage these risks by measuring financed emissions, which reflect their exposure to climate-related risks and potential necessary adaptations over time.

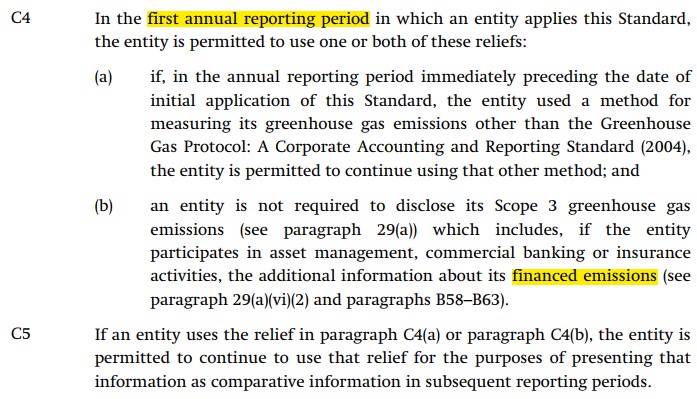

Paragraph 29(a)(i)(3) mandates entities to disclose their total gross Scope 3 greenhouse gas emissions from the reporting period, encompassing both upstream and downstream emissions. Entities involved in asset management, commercial banking, or insurance are required to disclose additional information about their Category 15 financed emissions.

Asset management category 15 additional diclosures | IFRSS2.B61

Entities with asset management operations are required to disclose the following additional information with respect to their category 15 financed emissions:

(Illustrative 29(a) Category 15 disclosures) |

Scope 1 emissions |

Scope 2 emissions |

Scope 3 emissions |

(a) Absolute gross financed emissions |

23 tonnes C02E |

910 tonnes C02E |

2576 tonnes C02E |

(b) Assets under management included in financed emissions disclosure |

Euro600bn |

Euro600bn |

Euro600bn |

(c) % of entity's total AuM included in financed emissions calculation (if less than 100% explain the types of assets excluded & their associated AuM) |

100% |

100% |

100% |

(d) Method used to calculate financed emissions, including the method of allocation the entity used to attribute its share of emissions in relation to the size of investments. |

Direct measurement and equity share methods were used. |

CO2E is Carbon dioxide equivalent

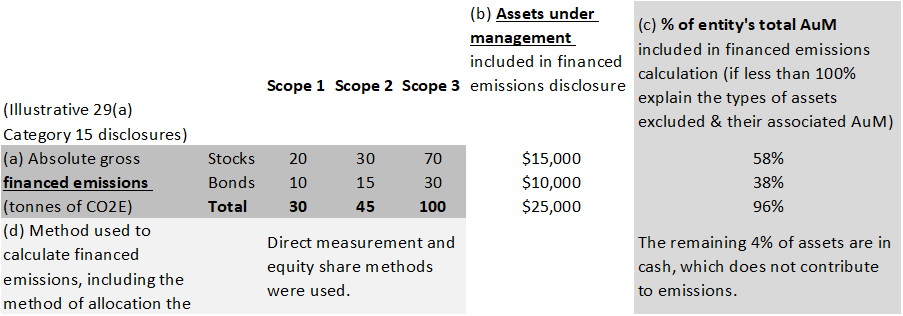

Disaggregation by asset class

Consider an asset manager with funds under management across multiple portfolios of bonds and stocks, which aggregate to:

- Stocks : $15bn

- Bonds : $10bn

- Cash : $1bn

The asset manager reports carbon emissions linked to stocks and bonds, but assesses that the assets in cash don't contribute to emissions.

Whilst asset managers are not required by IFRS S2 to disaggregate their emissions by asset class, IFRS S1 B29-B30 requires consideration of whether presenting the data in an aggregated format conceals material information. The entity considers that bonds and stocks are affected differently by climate-related risks and opportunities.

Despite no rule specifying a split of carbon emissions by bonds and stocks, the firm does so:

Disaggregation by active/passive investment strategies

An asset manager may offer both active as well as passive investment strategies. When the asset manager does its IFRS S2 paragraph 29(a) emissions disclosures; it will consider whether the principles of aggregation and disaggregation in IFRS S2 (B29 and B30) require it to disaggregate emissions from active and passive investment strategies.

An asset manager may offer both active as well as passive investment strategies. When the asset manager does its IFRS S2 paragraph 29(a) emissions disclosures; it will consider whether the principles of aggregation and disaggregation in IFRS S2 (B29 and B30) require it to disaggregate emissions from active and passive investment strategies.

The asset manager shall consider:

- Are the active management fees significantly higher than the passive management fees? Which contribute more to revenue? Is this expected to change?

- Are the greenhouse gas emissions of its active management strategies significantly different to those of its passive strategies?

- The active strategies may have greater flexibility than the passive strategies, in managing or reducing their financed emissions.

Although IFRS S2 does not explicitly require an asset manager to disclose its passive strategy emissions seperately to its active strategy emissions; IFRS S1 B29-B30 prohibit information from being aggregated if doing so would obscure info that is material.

Although IFRS S2 does not explicitly require an asset manager to disclose its passive strategy emissions seperately to its active strategy emissions; IFRS S1 B29-B30 prohibit information from being aggregated if doing so would obscure info that is material.

For the reasons above, asset managers may want to disaggregate their disclosures of paragraph 29(a) emissions between active and passive investment strategies.

Commercial banking | IFRSS2.B62

Entities which participate in commercial banking activity need to report financed emissions seperately for each industry and each asset class:

- Using the "Global Industry Classification Standard" (GICS) 6-digit industry-level code for classifying counterparties into the various industries:

- 101010 Energy Equipment & Services

- 101020 Oil, Gas & Consumable Fuels

- 151010 Chemicals

- 151020 Construction Materials

- 151030 Containers & Packaging

- 151040 Metals & Mining

- 151050 Paper & Forest Products

- 201010 Aerospace & Defense

- 201020 Building Products

- 201030 Construction & Engineering

- 201040 Electrical Equipment

- 201050 Industrial Conglomerates

- 201060 Machinery

- 201070 Trading Companies & Distributors

- 202010 Commercial Services & Supplies

- 202020 Professional Services

- 203010 Air Freight & Logistics

- 203020 Passenger Airlines (New name)

- 203030 Marine Transportation (New Name)

- 203040 Ground Transportation (New Name)

- 203050 Transportation Infrastructure

- 251010 Automobile Components (New Name)

- 251020 Automobiles

- 252010 Household Durables

- 252020 Leisure Products

- 252030 Textiles, Apparel & Luxury Goods

- 253010 Hotels, Restaurants & Leisure

- 253020 Diversified Consumer Services

- 255010 Distributors

- 255020 Internet & Direct Marketing Retail (Discontinued)

- 255030 Broadline Retail (New Name)

- 255040 Specialty Retail

- 301010 Consumer Staples Distribution & Retail (New Name)

- 302010 Beverages

- 302020 Food Products

- 302030 Tobacco

- 303010 Household Products

- 303020 Personal Care Products (New Name)

- 351010 Health Care Equipment & Supplies

- 351020 Health Care Providers & Services

- 351030 Health Care Technology

- 352010 Biotechnology=

- 352020 Pharmaceuticals

- 352030 Life Sciences Tools & Services

- 401010 Banks

- 401020 Thrifts & Mortgage Finance (Discontinued)

- 402010 Financial Services (New Name)

- 402020 Consumer Finance

- 402030 Capital Markets

- 402040 "Mortgage Real Estate Investment Trusts (REITs)"

- 403010 Insurance

- 451020 IT Services

- 451030 Software

- 452010 Communications Equipment

- 452020 Technology Hardware, Storage & Peripherals

- 452030 Electronic Equipment, Instruments & Components

- 453010 Semiconductors & Semiconductor Equipment

- 501010 Diversified Telecommunication Services

- 501020 Wireless Telecommunication Services

- 502010 Media

- 502020 Entertainment

- 502030 Interactive Media & Services

- 551010 Electric Utilities

- 551020 Gas Utilities

- 551030 Multi-Utilities

- 551040 Water Utilities

- 551050 Independent Power and Renewable Electricity Producers

- 601010 Diversified REITs (New Name)

- 601025 Industrial REITs (New)

- 601030 Hotel & Resort REITs (New)

- 601040 Office REITs (New)

- 601050 Health Care REITs (New)

- 601060 Residential REITs (New)

- 601070 Retail REITs (New)

- 601080 Specialized REITs (New)

- 602010 Real Estate Management & Development (New Code)

- IFRS S2 lists the following asset classes :

- loans,

- project finance,

- bonds,

- equity investments and

- undrawn loan commitments

If the commercial bank discloses financed emissions for other asset classes, it shall substantiate why the inclusion of those additional asset classes provides relevant information.

So here's an illustrative example of what a bank must report for each industry and asset class, e.g. :

GICS code: 251020 Automobiles

Asset class:

equity investments |

Scope 1 emissions |

Scope 2 emissions |

Scope 3 emissions |

Absolute gross financed emissions |

23 tonnes C02E |

910 tonnes C02E |

2576 tonnes C02E |

Funded carrying amounts* |

Euro600bn |

Euro600bn |

Euro600bn |

| Undrawn loan commitments* |

Euro700bn |

Euro100bn |

Euro300bn |

% of gross exposure included in financed

emissions calculation. (if less than 100% explain the exclusions including the types of assets excluded) |

100% |

100% |

100% |

% of undrawn loan commitments included in financed emissions calculation. |

100% |

100% |

100% |

Method used to calculate financed emissions, including the method of allocation the entity used to attribute its share of emissions in relation to the size of its gross exposure. |

Direct measurement and control approach methods were used. |

* Funded carrying amounts are before subtracting the loss allowance, when applicable, whether prepared in accordance with IFRS Accounting Standards or other GAAP. For funded amounts, exclude from gross exposure all impacts of risk mitigants, if applicable

Insurance | IFRSS2.B63

Entities which participate in insurance-related activities need to report financed emissions seperately for each industry and each asset class:

- loans,

- bonds,

- equity investments and

- undrawn loan commitments

- (the only difference for an insurer vs a commercial bank, is that project finance isn't automatically included as an asset class)

If the insurer discloses financed emissions for other asset classes, it shall substantiate why the inclusion of those additional asset classes provides relevant information.

So here's an illustrative example of what an insurer must report for each industry and asset class, e.g. :

GICS code: 251020 Automobiles

Asset class:

equity investments |

Scope 1 emissions |

Scope 2 emissions |

Scope 3 emissions |

Absolute gross financed emissions |

23 tonnes C02E |

910 tonnes C02E |

2576 tonnes C02E |

Funded carrying amounts* |

Euro600bn |

Euro600bn |

Euro600bn |

| Undrawn loan commitments* |

Euro700bn |

Euro100bn |

Euro300bn |

% of gross exposure included in financed

emissions calculation. (if less than 100% explain the exclusions including the types of assets excluded) |

100% |

100% |

100% |

% of undrawn loan commitments included in financed emissions calculation. |

100% |

100% |

100% |

Method used to calculate financed emissions, including the method of allocation the entity used to attribute its share of emissions in relation to the size of its gross exposure. |

Direct measurement and control approach methods were used. |

* Funded carrying amounts are before subtracting the loss allowance, when applicable, whether prepared in accordance with IFRS Accounting Standards or other GAAP. For funded amounts, exclude from gross exposure all impacts of risk mitigants, if applicable

Resources

IFRS S2 reference documents