Climate-related targets | IFRS S2

See IFRSS2.33-37

In identifying and disclosing the metrics to use to define climate-related targets and monitor progress, an entity should take into account the applicability of:

- cross-industry metrics (IFRSS2.29) and

- industry-based metrics (IFRSS2.32).

If the metric has been developed to measure progress towards a target, info should be disclosed about that metric in accordance with IFRSS1.50.

If the metric has been developed to measure progress towards a target, info should be disclosed about that metric in accordance with IFRSS1.50.

The entity shall disclose for each target, quantitative or qualitative, internal or regulatory (including emissions), the following info about the characteristics of each target:

- Metric used;

- Objective of the target (mitigation, adaption or conformance with science-based initiatives);

- Part of entity to which target applies (e.g. specific business units, geographies or the entirety)

- Period over which the target applies;

- Base period from which progress is measured;

- Any milestones & interim targets;

- If quantitative, whether it is:

- an absolute target (a total amount of a measure or a change in the total amount of a measure) or

- an intensity target (a ratio of a measure, or a change in the ratio of a measure, to a business metric )

- How the latest international agreement on climate change, including jurisdictional commitments that arise from that agreement, has informed the target.

Setting & reviewing targets

The approach to setting & reviewing each target shall be disclosed, and how progress is monitored:

- Was a 3rd party involved in setting the target or validating it?

- What is the process for reviewing the target?

- What metrics are used to monitor progress towards meeting the target?

- Any revisions to the target and why.

Disclose the performance against each target & provide an analysis of trends or changes in the entity’s performance.

For each greenhouse gas target, disclose

For each greenhouse gas target, disclose

- Which greenhouse gases are covered.

- Whether scope 1, 2 or 3 emissions are covered.

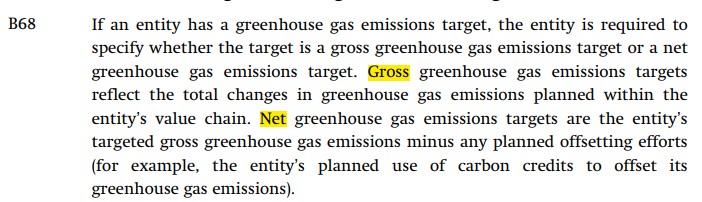

- Is it a gross or net emissions target? If net, the associated gross target must also be disclosed.

- Was it derived using a sectoral decarbonization approach?

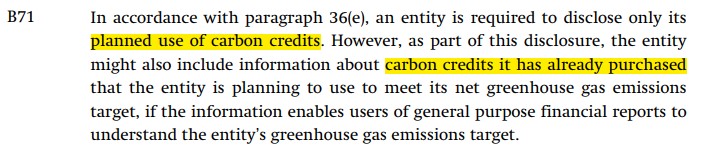

- Planned use of carbon credits (which are transferable or tradeable instruments)

to offset emissions to achieve target, including:

extent to which achieving the net ghg emissions target relies on the use of carbon creditr;

extent to which achieving the net ghg emissions target relies on the use of carbon creditr;- which 3rd party scheme will verify or certify the carbon credits

- type of carbon credit, is the underlying offset nature-based or based on technological carbon removals; is the underlying offset achieved through carbon reduction or removal.

- any of factors necessary to understand the credibility & integrity of the carbon credits the entity plans to use (e.g. assumptions about the permanence of the carbon offset).

Resources

Click here.