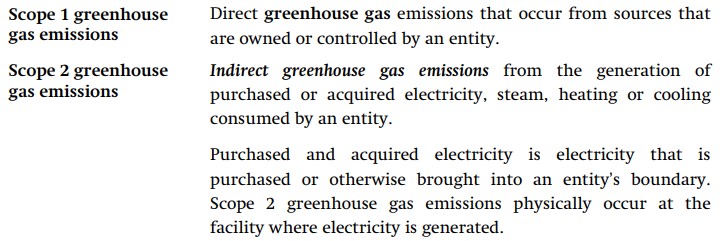

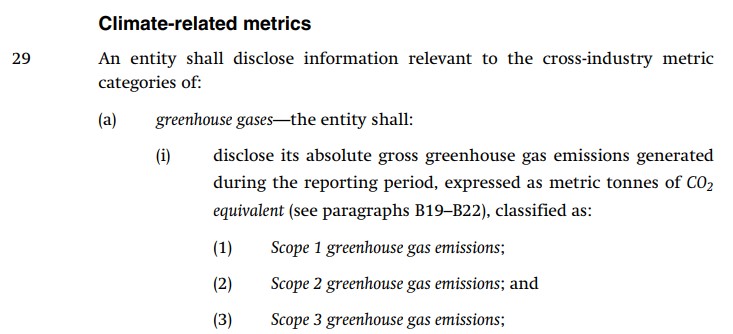

See IFRSS2.29 and definitions

Scope 3 greenhouse gas emissions are defined in the IFRS S2 standard as being "Indirect greenhouse gas emissions (not included in Scope 2 greenhouse gas emissions) that occur in the value chain of an entity, including both upstream and downstream emissions. Scope 3 greenhouse gas emissions include the Scope 3 categories in the Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (2011)."

1. Purchased goods and services

2. Capital goods

3. Fuel- and energy-related activities(not included in scope 1 or scope 2)

4. Upstream transportation and distribution

5. Waste generated in operations

6. Business travel

7. Employee commuting

8. Upstream leased assets

9. Downstream transportation and distribution

10. Processing of sold products

11. Use of sold products

12. End-of-life treatment of sold products

13. Downstream leased assets

14. Franchises

15. Investments (additional info required if entity’s activities include asset management, commercial banking or insurance (see paragraphs B58-B63);

Paragraph 29 disclosure requirements

Paragraph 29 disclosure requirementsParagraph 29 of IFRS S2 requires an entity to disclose its scope 3 emissions, and paragraph 29(a)(vi) requires disclosures of:

the categories included as per the Greenhouse Gas

Protocol Corporate Value Chain (Scope 3) Accounting

and Reporting Standard (2011); and

additional information about Category 15

greenhouse gas emissions or those associated with its

investments (financed emissions), if the entity's activities

include asset management, commercial banking or

insurance (see paragraphs B58-B63);

Example : disaggregation of Scope 3 disclosures into categories

Example : disaggregation of Scope 3 disclosures into categoriesConsider an entity which has greenhouse gas emissions from:

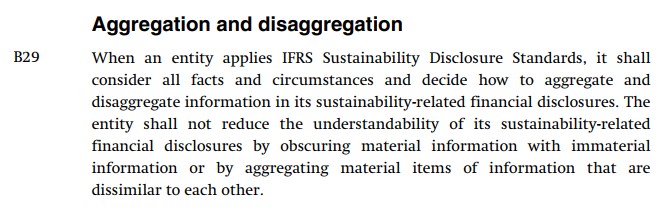

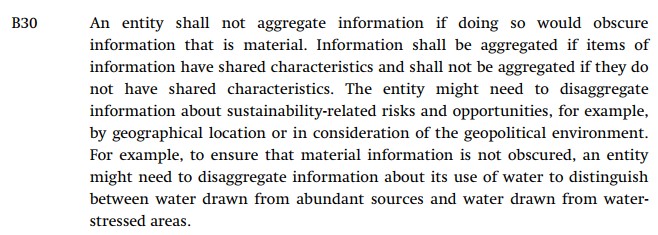

The entity will consider whether it should disaggregate its emissions disclosures into those categories, as per the requirements of IFRSS1.B29-B30.

With respect to category 6, business travel, the entity considers that:

With respect to category 10, processing of sold products, the entity considers that:

Although IFRS S2 does not explicitly require disaggregation of scope 3 emissions, the entity considers the requirement in IFRS S1 that prohibits info from being aggregated if doing so would obscure info that is material.

The entity therefore determines that disaggregating info about its scope 3 category 10 ghg emissions is necessary to provide material info to users of general purposes financial reports; and decides to provide a table to supplement the paragraph 29(a) disclosure of its scope 3 ghg emissions:

An entity is a leading multinational technology company known for producing consumer electronics, software, and digital services. Its diverse product portfolio includes smartphones, tablets, laptops, smartwatches, and various smart home devices.

The entity calculates its greenhouse gas emissions (Scope 3 Category 4) related to upstream transportation and distribution, specifically emissions resulting from the transportation of purchased goods and services.

The entity is deliberating on whether to disclose detailed information about the individual greenhouse gases (CO2, methane, and nitrous oxide) emitted during upstream transportation and distribution activities or provide a more generalized view of emissions in this category (although not explicitly required by IFRS S2 to disaggregate Scope 3 Category 4 greenhouse gas emissions by constituent ghg, the entity considers the requirement in IFRS S1 that prohibits info from being aggregated if doing so would obscure information that is material).

Key considerations influencing this decision include:

Data Availability and Accuracy: The entity needs to assess whether it has accurate and reliable data on emissions of CO2, methane, and nitrous oxide during transportation and distribution. If data is readily available and can be accurately measured, disclosing specific greenhouse gases might provide a more comprehensive picture of the environmental impact.

Industry-based guidance: The entity is required to refer to and consider the applicability of "Volume 5 - Household & Personal Products" of the Industry-based Guidance on Implementing IFRS S2.

Materiality: The entity must determine if emissions of CO2, methane, and nitrous oxide are material to its overall greenhouse gas emissions profile. If these gases contribute significantly to the entity's carbon footprint within Scope 3 Category 4, their disclosure becomes more relevant and valuable for stakeholders.

Stakeholder Expectations: The entity should consider the expectations of its stakeholders, such as investors, customers, and regulators. If stakeholders are specifically interested in the breakdown of emissions by individual greenhouse gases, the entity may choose to disclose this information to meet those expectations.

Regulatory Requirements: The entity needs to be aware of any reporting requirements or guidelines from regulatory bodies that mandate the disclosure of specific greenhouse gases. If such requirements exist, the entity should comply with them accordingly.

Transparency and Accountability: Providing detailed information on CO2, methane, and nitrous oxide emissions can demonstrate the entity's commitment to transparency, environmental responsibility, and sustainability goals.

Based on these considerations, the entity determines that it is necessary and appropriate to disclose CO2, methane, and nitrous oxide emissions separately, to provide material info to users of general purpose financial reports.

The entity produces the following table to supplement its 29(a) emissions disclosures: